Reporting entities should continue to use existing guidance notes and information sheets for reporting periods that began prior to 1 July 2024.

Update September 2024

The Regulator is updating its guidance materials for the new Payment Times Reporting Scheme.

We will consult on the process so people can engage with the Regulator and understand the new requirements.

Download

INFO5: Acquisitions, divestments and winding up [PDF 599 kB]

Contents

- Acquisitions and divestments

- Winding up

- Ceasing to be a constitutionally covered entity

- Further information

Guidance for entities that are subject to a change of control or have ceased to exist and help with the impact on reporting under the Payment Times Reporting Scheme.

Acquisitions and divestments

This information sheet provides general guidance only and does not amount to legal advice. Entities are encouraged to seek independent legal advice to clarify their rights and obligations under the Act.

Changes in control of an entity can impact the reporting obligations of both the acquired entity and its acquirer. New obligations can also arise where entities are acquired by a corporate group and therefore, need to apply a different income threshold.

Below is general guidance and practical examples of how acquisitions and divestments can affect reporting obligations.

General guidance

The impact a change of control will have on reporting will depend on the circumstances of the acquirer and acquired entity at the time of the change of control, but general principles can be applied.

General guidance for changes in control

| Individual reporting entities have the obligation to report | Although controlling corporations and head entities can report on behalf of their entities, the obligation to report is on each individual reporting entity for each reporting period. There is no obligation for an entity to report on behalf of another entity. An entity does not have an obligation to report on behalf of former member entities or subsidiaries that have been divested from a corporate group. The obligation to report remains with the divested entity. | See Guidance note 2: Preparing a payment times report [6]-[9] |

| The commencement of reporting obligations depends on existing obligations | Entities that are already reporting entities at the time of a change of control, continue to report according to their existing obligations until they cease to be reporting entities. Entities that are not reporting entities at the time of a change of control, assess their reporting obligations at the commencement of their next income year. | See Guidance note 1: Key concepts at [5] and [36]-[37] |

| Entities continue to report according to their income year | An entity may change its income year to align with a new parent entity following a change of control. Entities must continue to report according to their existing income year until it is changed for tax reporting purposes. In some cases, we will register a report covering only part of a reporting period if it helps alignment. Entities should not ‘split’ a reporting period into separate reports pre and post transaction. Entities should continue to submit one report for each reporting period. | See Guidance note 1: Key concepts at [66]-[70] |

| Changes in control can affect applicable income thresholds | Where the acquirer and acquired entity are both incorporated, the transaction may create a controlling corporation and member relationship for the purposes of reporting. This can impact the income thresholds applicable to entities in the group and the information required to be given in a report. | See Information sheet 4: Corporate groups |

| Entities may need to report the change in control | Reporting entities are required to include information in their payment times reports that provide context and explanation to their report. In general, this should include details of a change of control in the Report comments section. | Guidance note 2: Preparing a payment times report at [30]-[32] |

Timing and impact on obligations

A change of control may affect what needs to be reported for a reporting period but does not change or modify the entity’s existing status or obligations as a reporting entity:

- An entity can only become a reporting entity at the beginning of an income year and can only cease to be a reporting entity in accordance with the Act.

- A change in control during a reporting period does not change an entity’s existing status as a reporting entity in that reporting period.

- If a change occurs during a reporting period, the entity should report based on its circumstances as at the end of the reporting period, not as of the date the report is submitted (see example below).

- Changes in control for reporting entities should be reflected in the report comments in the reporting period where the change occurred.

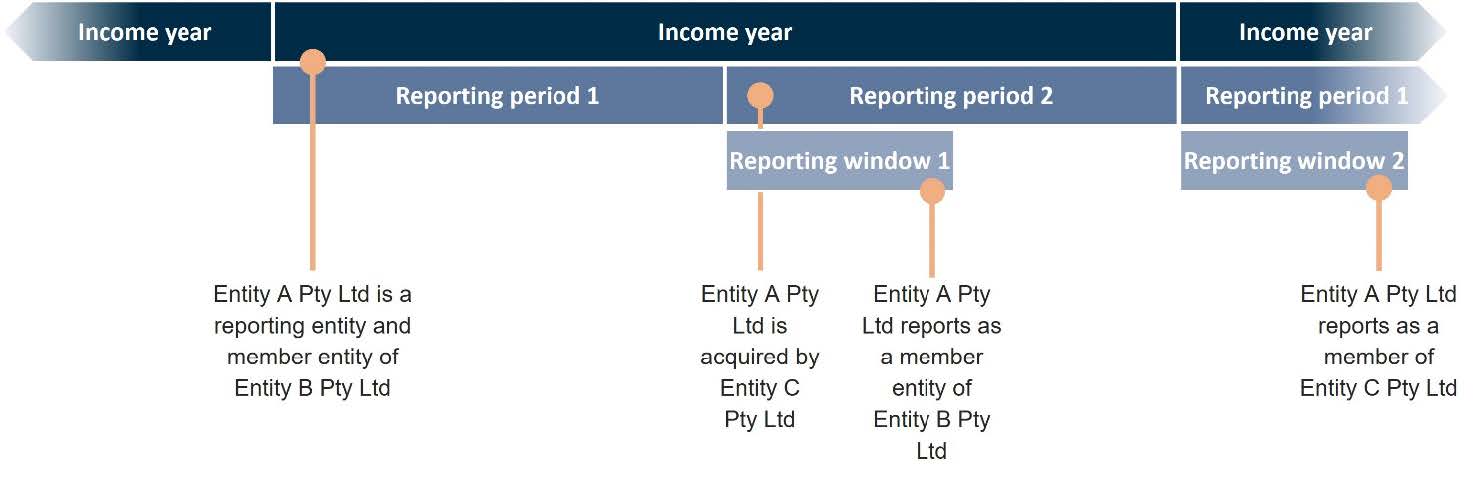

Example – Reporting entity change of control

Guidance for member entities

Member entities are required to apply two income thresholds: first, the total aggregate income of their corporate group, and second, their individual income. Because of this, a change in control can impact member entities differently to entities that only apply the general income threshold of A$100 million.

General guidance for member entities

| Where a controlling corporation becomes a member entity following a change in control and… | |

| The total aggregate income of the acquiring group is greater than A$100 million and the entity’s income is greater than A$10 million. | Continue to report as a member entity and include information in the report comments regarding the change from controlling corporation to being a member entity. |

The total aggregate income of the acquiring group is less than A$100 million. OR The entity’s income is less than A$10 million. | Continue to report until they cease to be a reporting entity. The entity may make an application for a determination to cease to be a reporting entity (see Guidance Note 3 – Applications and notifications). |

| Where a member entity becomes a member entity of another controlling corporation following a change in control and… | |

| It was not a reporting entity at the time of the change of control. | Continue to assess whether they have become a reporting entity at the beginning of each income year. |

| It was a reporting entity at the time of the change of control and the acquiring group has total aggregate group income greater than A$100 million. | Continue to report as a member entity in the new corporate group. |

| It was a reporting entity at the time of the change of control and the acquiring group has total aggregate group income less than A$100 million | Continue to report until they cease to be a reporting entity. The entity may make an application for a determination to cease to be a reporting entity (see Guidance Note 3 – Applications and notifications) |

Winding up

Reporting entities are required to submit a payment times report until they cease to be reporting entities, in accordance with the Payment Times Reporting Act 2020.

An exception to this is where an entity has ceased to exist because has been wound up or deregistered. Where an entity ceases to have separate legal status, its reporting obligations cease. For clarity, this only applies where an entity has been wound up or deregistered. Entities cannot cease reporting just because they have ceased operating or intend on winding up.

Although an entity is not required to submit a report for the reporting period in which it was wound up, it should consider:

- revising its most recent payment times report to include comments that it will be the entity’s final report and the reasons why

- logging in to the Payment Times Reporting Portal and updating its details. See Guidance Note 3: Applications and notifications.

If entities do not make these changes, they may continue to receive reporting and compliance communications.

Outstanding reports

Entities should ensure they do not have outstanding payment times reports at the time of winding up. For some entity types, failure to submit outstanding reports may result in compliance action against other entities and individuals responsible for the entity that was wound up: see Guidance Note 1 – Key concepts.

Ceasing to be a constitutionally covered entity

An entity’s circumstances may change, resulting in it no longer being a constitutionally covered entity. This is most likely to occur where an entity is only a constitutionally covered entity because it carries on an enterprise in a Territory, and it ceases all activities in that Territory: see Information Sheet 3 – Who must report and Guidance Note 1 – Key concepts.

Entities that are not constitutionally covered entities cannot be reporting entities: see Information Sheet 3 – Who must report and Guidance Note 1 – Key concepts.

If an entity’s circumstances change so that it is no longer a constitutionally covered entity, it should consider following the same process as recommended for entities winding up or it may continue to receive reporting and compliance communications.

Further information

For more information, please refer to the additional guidance notes and information sheets available in the Guidance section of the Payment Times Reporting Regulator’s website.